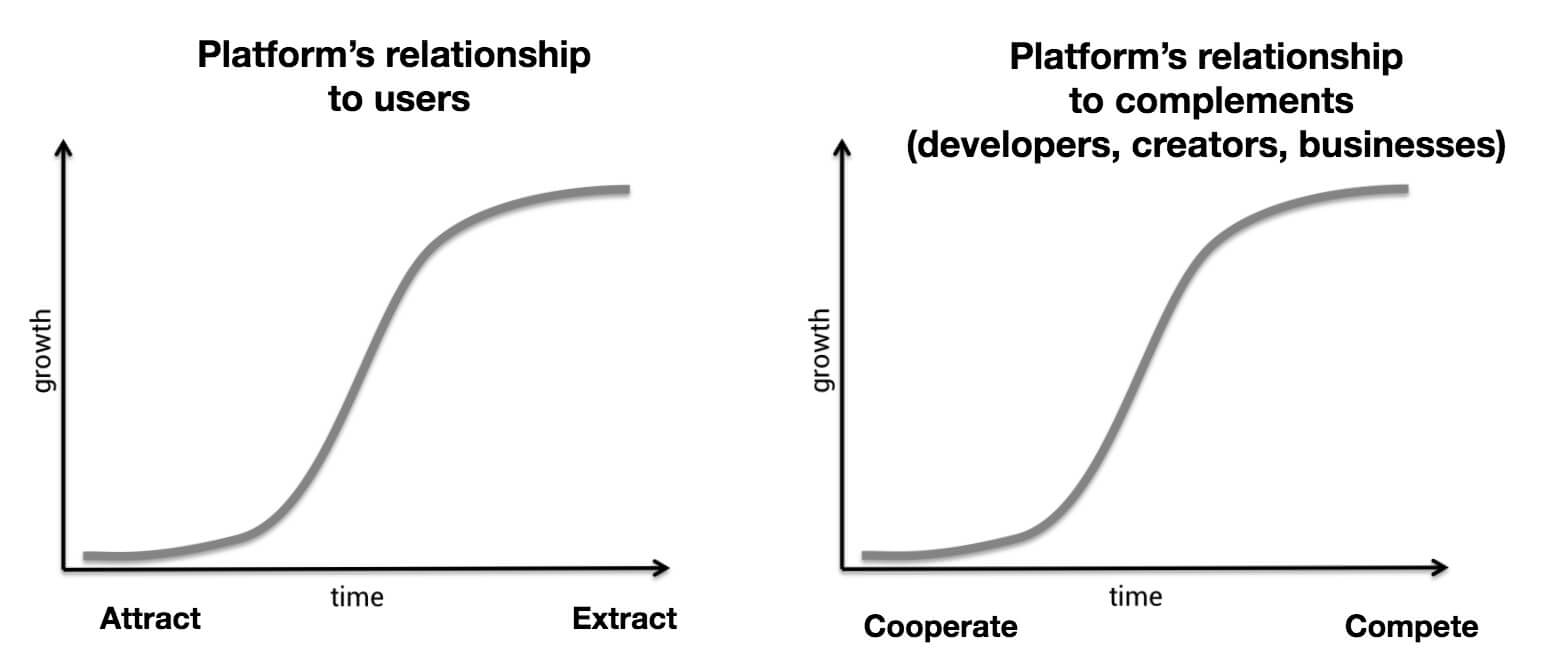

Today, some of the most valuable corporations in the world today are “network operators”. Thanks to network effects, these platforms become more valuable to existing users as each new user joins. Network effects are innocuous at first, but can cause concern at scale if platforms enter an “extractive” phase in their lifecycle. My partner Chris has illustrated the evolution of platforms with network effects — and their relationships to their users — as follows:

The key phenomenon to note above is that these platforms shift from cooperating with their users (“complements”/ complimentary businesses in economic terms), to competing with them.

But what if there were a way for platforms to commit to continued cooperation? To support unabated, independent entrepreneurial activity — as well as an improved user experience — for all the participants who depend on the network?

While people have suggested everything from regulating networks as public utilities to mandating that they provide open APIs, we believe that cryptonetworks — what we call “community owned and operated networks” — could unlock a new paradigm for continued cooperation, while still sustaining strong network effects.

Cryptonetworks are a relatively new phenomenon, but there’s a useful analog to help understand why they work and where they’re going: cooperatives, or “co-ops”. It may also be a helpful analogy for those seeking how to explain crypto to newcomers.

What if there were a way for platforms to commit to continued cooperation?

The rise of the co-op: not just for social reasons, but good for business

Cooperatives are participatory enterprises that are owned and operated by their members. Members can be the creators, or the consumers, of the cooperative’s product or service; for instance, Arizmendi Pizza is a co-op where all the pizza makers also operate and own the business (and probably consume it, too). Or, take the example of REI — a consumer cooperative with revenues of $2.9B — where consumers, not just shareholders, also earn a dividend based on the purchases they make.

Cooperatives differ from traditional companies in that they are typically funded by direct member investment, rather than investment from third-party shareholders. This allows members to decide on the values of the enterprise, which don’t necessarily need to be about the maximization of profits. In fact, cooperatives tend to be most successful where there’s alignment on other values such as: 1) a communal benefit to pooling resources, for economies of scale; and 2) an attendant desire to avoid anti-competitive or extractive behavior.

Upholding a commitment to these values isn’t merely a social endeavor — it can be good for business too, both in terms of direct return on investment and downstream value creation. This is true because as a cooperative grows, it takes on economies of scale that can increase the value of membership for all participants. Early participants can use their newfound surplus for additional access to the product or service (creating more downstream value), or take profits by selling surplus to new members to earn a return (the direct investment value).

According to the International Co-op Alliance, cooperatives are not just marginal phenomena — at least 12% of the population is in “cooperatives”; co-ops “provide jobs or work opportunities to 10% of the employed population”; and the 300 top coops and groups also generate $2.1 trillion “in turnover while providing the services and infrastructure society needs to thrive”.

Those are just some of the numbers. In terms of success, perhaps the most famous example of a cooperative is Visa, given its origin story. Originally part of Bank of America (and called BankAmericard), the credit card network struggled to gain the ubiquity required for widespread consumer adoption. So BankAmericard (later Visa) was spun out into a member-owned consortium that incentivized competitive banks to join. This grew the network effects of the platform, while protecting the individual members from fees that could be extracted had a centralized third party aggregated them instead. Today, VISA is worth more than the sum of its individual members, who benefited when the company went public.

Many stock exchanges were also conceived as member-operated platforms. Owning a seat on The New York Stock Exchange was mandatory to trade, but also offered reassurance that the power of pooled liquidity could not be used to extract high fees from traders later on. Industries such as mutual insurance, credit unions, housing, agriculture, and many others have successful cooperative ownership structures. There are example of co-ops in everything from dairy — Land O’Lakes is a cooperative with a market value of $22.5 billion — to mutual funds (another variant of a member-owned enterprise); Vanguard is structured so “…there are no outside owners, and therefore, no conflicting loyalties.”

Where co-ops fall short

Aligned incentives means a mutual like Vanguard never has to “weigh what’s best for clients against what’s best for the company’s owners, because they are one and the same”. But when it comes to innovation, there are some structural issues that have worked against cooperative enterprises, from coordination costs to growth to governance.

For instance, cooperatives are more difficult to bootstrap than corporations because they don’t have access to the same capital markets. Historically, it’s been a lot harder to coordinate investment from members with shared values than it is to raise funds with the singular goal of maximizing profits. There are also logistical challenges in everything from distributing information to bootstrapping the co-op so that it reaches a minimum viable threshold where it actually delivers utility to its members.

Then, even once over the bootstrap hump, cooperatives can struggle to compete with more traditional entrants, who are often better funded. For example, in the early 1990s, many member-owned stock exchanges elected to “demutualize” or convert from member-owned organizations to for-profit, investor-owned ones (Visa did this as well when it went public). This coincided with the advance of the internet, which democratized access to markets and increased competition.

Finally, cooperatives tend to have more complex governance processes than companies with simple top-down management structures. The challenge for co-ops is to ensure that the often pluralist values of their members are accurately represented and upheld, while also preserving operational efficiency. Many successful cooperatives have therefore combined formal management hierarchies with thoughtful permissioning by members (as opposed to flat, direct democracies).

Cooperative networks: thoughts for crypto

While policymakers (and users) around the world debate whether internet networks should be regulated as public utilities, cryptonetworks are pioneering a new form of “cooperative capitalism” with networks that are owned by users and workers, rather than by third-party shareholders. In this way cryptonetworks share many features of cooperatives. Beyond the ability to crowdsource funds from members of the network, cryptonetworks can compete with better capitalized corporations on other dimensions — especially those that require high degrees of trust.

Because cryptonetworks are information networks based open source code, shared state, automated “smart contracts”, and 24/7 international markets — all tools that allow participants to find one another, share information, and coordinate — these networks can more easily get past the bootstrap hump that cooperative enterprises traditionally face. By encoding commitments to continued cooperation in software, cryptonetworks can engender trust at new scales, both granular (due to cost efficiencies) and macro (due to social scalability).

Another dimension on which cryptonetworks can compete is growth: Networks that treat their users equitably may be easier and cheaper to grow, as early participants are incentivized to drive network effects, because they can participate in the value they help create. This trend aligns with a broader movement towards stakeholder inclusion, with companies like Airbnb and Uber petitioning to grant stock options to suppliers in their networks.

Finally, cryptonetworks open new territory to explore how cooperative governance can be both efficient andrepresentative. While these have often been viewed competing goals, software-based governance mechanismsoffer new tools to address this tension.

Cryptonetworks open new territory to explore how cooperative governance can be both efficient and representative

But what what will it take to scale cooperative governance, without centralized privatization or government intervention? If we think of both co-ops and cryptonetworks as “commons”, then tactics for governing their resources require these three necessary conditions (as proposed by Elinor Ostrom in Governing the Commons):

- An institution of rules

- A credible commitment to follow them (generally, the ability to punish)

- And collective monitoring to ensure rules are upheld and commitments actioned upon.

Both Bitcoin and Ethereum already meet these criteria by combining the verifiable-by-math nature of cryptography with new economic mechanisms that incent the work necessary to maintain the services:

- Rules are programmatic (open source code);

- Credible commitments are economic, pledged in the form electricity in Proof-of-Work mining, or deposited bonds in Proof-of-Stake systems, plus rewards for following the rules;

- Collective monitoring is performed by nodes that can verify that the rules have been followed, deterministically.

These foundations provide a new toolkit for cooperative governance of a common resource. The challenge, of course, will be addressing how these tools evolve as the networks themselves do, and as the services layered on top become more intricate: Rules will need to be updated; commitments will become more diffuse and difficult to measure; and monitoring will shift from machine-verifiable processes towards more subjective, human ones. For example, credible commitments might need to be both economic and social, with the latter pledged in the form of identity and reputation as a supplement to capital expenditure.

So while software opens up a new design space for experiments in cooperative governance, we’ll need to be rigorous in thinking through how these networks can be robust in the face of increased complexity. Here, the history of cooperative governance structures — both in their successes and their failures — may be a useful analog, and inspiration, for those building new networks and applications. These networks are made of people, after all, only now they’re empowered by cryptography, programmable money, open source code, open data, and markets for the best ideas to win.

Thanks to Denis Nazarov, Chris Dixon, Sonal Chokshi, and Toby Shorin for feedback on this post.

This post originally appeared on a16z.com

The views expressed herein are those of the individual personnel quoted herein and are not the views of AHCM or its affiliates. This presentation is provided solely for informational purposes and should not be relied upon when making any investment decision. References to any securities or digital assets are for illustrative purposes only and do not constitute a recommendation to invest in any instrument nor do they constitute an offer to provide investment advisory services.

This content should not be relied upon as legal, business, investment or tax advice. You should consult your own advisers as to legal, business, tax and other related matters concerning any investment. Furthermore, this content is not directed at nor intended for use by any investor or prospective investor, and may not under any circumstances be relied upon when making a decision to invest in any fund.

Past performance is not indicative of future results. Charts and graphs provided herein are for informational purposes only and should not be relied upon when making any investment decision. Please see https://a16z.com/disclosures for additional important information.